When we talk about the levers of economic power, none are quite as heavy—or as politically charged—as fiscal policy. Far more than a simple spreadsheet of numbers, a national budget represents a government’s values codified into currency. It tells the story of who gets taxed, who gets support, and how much of the burden is shifted onto future generations.

As we navigate 2026, the era of easy money appears to be over. With interest rates hovering significantly higher than the near-zero levels of the 2010s, the cost of servicing national debt is rising, forcing governments to face difficult trade-offs between stimulus, austerity, and simply paying the bills.

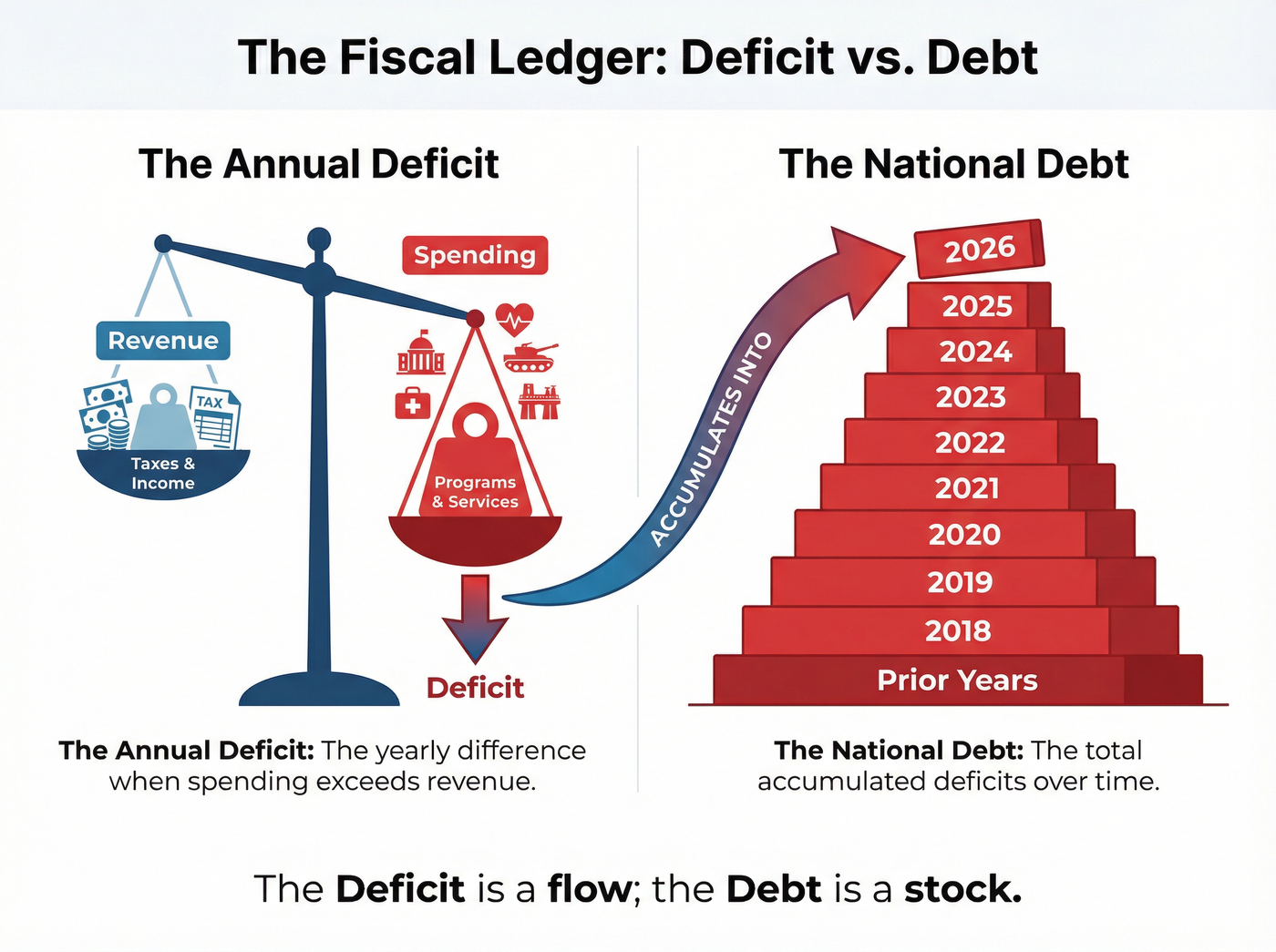

The Distinction Between Deficits and Debt

In casual conversation, the terms "deficit" and "debt" are often thrown around interchangeably, but the economic distinction is vital. The budget deficit is a flow variable—it represents how much more the government spends than it accounts for in tax revenue within a single fiscal year. It is the immediate "this year" problem.

The national debt, conversely, is a stock variable. It is the accumulated mountain of all past deficits. Think of it like a credit card: the deficit is the amount you overspend in one month, while the debt is the total balance you owe the bank. As of early 2026, the scale of this balance is becoming historic. According to a preliminary review of the February 2026 Congressional Budget Office (CBO) outlook, publicly held debt in the United States is projected to hit 120 percent of GDP by 2036.[1]

This projection signals a fundamental shift. For decades, governments could borrow cheaply. Today, however, the rising cost of servicing this massive debt is consuming a larger share of the budget, leaving less money for infrastructure, education, and defense.

The Mechanisms of Spending: Guardrails and Gas Pedals

Fiscal policy operates through two main channels: automatic stabilizers and discretionary policy.

Automatic stabilizers are the economy's silent guardians. These are pre-coded mechanisms in the tax and transfer system—such as progressive tax rates and unemployment benefits—that trigger immediately when the economy slows down. They provide a cushion without Congress needing to pass a single bill. By keeping money circulating when the private sector retreats, these stabilizers help prevent recessionary spirals.

Discretionary policy, on the other hand, involves active legislative changes, such as the passage of new stimulus packages or infrastructure bills. This is where the debate over the Keynesian multiplier takes center stage. The multiplier measures how much additional GDP is generated for every dollar the government spends. If the multiplier is greater than one, the spending effectively pays for itself in growth; if it is less than one, the spending may be inefficient or "crowd out" private investment.

The Threat of Fiscal Dominance

One of the more alarming developments in modern macroeconomics is the blurring line between fiscal and monetary policy. When a government’s debt becomes too large, the central bank may lose the independence to set interest rates based solely on inflation data. If raising rates to fight inflation would bankrup the government by making debt payments unaffordable, the central bank might be forced to keep rates artificially low.

This scenario is known as fiscal dominance. Recent analysis suggests this is no longer just a theoretical risk but a growing reality, as central banks face pressure to accommodate the treasury's need for cheap financing, potentially at the cost of higher long-term inflation.[4]

Sustainability and the "Spending Smarter" Imperative

Are we borrowing to invest, or borrowing to consume? This is the critical question defining debt sustainability. Economists argue that borrowing to fund productive assets—like high-speed rail, energy grids, or R&D—can generate enough future growth to service the debt. However, borrowing merely to pay for current services or interest on old debt is a path to stagnation.

Using the "fiscal gap" metric—which measures the policy changes needed to stabilize debt—recent research indicates the U.S. creates a substantial long-term imbalance. Projections suggest the debt-to-GDP ratio could reach a staggering 183 percent by 2054 if current laws remain unchanged.[6]

The International Monetary Fund (IMF) emphasizes that the solution isn't just about austerity; it is about spending smarter. Improving the efficiency of public investment ensures that state resources actually deliver economic returns rather than vanishing into administrative friction.[2] Furthermore, implementing robust "fiscal guardrails" can help governments commit to sustainable paths before market pressures force their hand.[3]

Local Impacts of Global Trends

The challenge of rising deficits is not unique to the U.S. federal government. Local and regional governments are also feeling the squeeze. For instance, British Columbia’s 2026/27 budget plan revealed a sharp spike in its deficit to $13.3 billion, driven by spending pressures that have outpaced revenue growth.[5] This illustrates how quickly "fiscal space"—the room a government has to maneuver during a crisis—can evaporate when structural deficits take hold.

As we look toward the 2030s, the margin for error is shrinking. The choices made today regarding taxation, entitlement reform, and public investment will determine whether national debts remain a manageable tool for growth or become a trap that stifles prosperity.

Listen to the episode

Dive deeper into the mechanics of government finance with Host Pely and guest Rhea in this full episode.

Sources

- A Preliminary Review & Analysis of the February 2026 CBO Budget and Economic Outlook

- IMF Fiscal Monitor (Oct 2025): Spending Smarter

- Fiscal Guardrails against Rising Debt and Looming Spending Pressures

- Indebted to the Printing Press: Fiscal Dominance Is No Longer Theoretical

- Deficits, Debt, and Tough Choices: Inside B.C.’s 2026/27 Budget Plan

- Auerbach & Gale: Fiscal Primer and Long-Term Projections